Eddie Dabdoub and the team at Dabdoub Law Firm won a landmark long-term disability insurance case in the11th Circuit Court of Appeals for a woman who suffered a stroke following a healthy pregnancy.

The case of Bradshaw v. Reliance Standard Life Insurance Company examines the interpretation of pre-existing condition provisions found in disability insurance policies, which often become a focal point of legal disputes.

Case Summary

Julissa Bradshaw, an employee covered under a group long-term disability (LTD) policy issued by Reliance Standard Life Insurance Company, became disabled due to complications arising from a stroke that occurred 9 days after she gave birth to a healthy baby girl.

At the time she became covered under the group LTD policy, she was already pregnant. While the policy was in effect, she had no complications during her pregnancy—it was a healthy pregnancy by all accounts.

Ms. Bradshaw began her pre-natal care on May 6, 2013. On November 4, 2013, she was diagnosed with preeclampsia and was scheduled to be induced on November 6, 2013. On November 8, 2013, she gave birth to a baby girl.

On November 17, 2013, Ms. Bradshaw went to the emergency room with complaints of headaches, dizziness, and nausea. An MRI of the brain completed at the time of admission revealed that she had suffered a massive infarct in the left cerebellar hemisphere – a stroke. She was immediately taken into surgery where the neurosurgeon performed a craniotomy to gain access to the cerebellar hemisphere where he then cut away (or “resected”) a portion of Bradshaw’s cerebellum.

On February 20, 2014, Ms. Bradshaw applied for LTD benefits, noting that she was unable to work due to pain, confusion, anxiety, dizziness, forgetfulness, and loss of coordination. Reliance Standard denied her long term disability claim citing the LTD policy's pre-existing condition exclusion, which included pregnancy as a pre-existing condition if medical treatment, consultation, care, or services were received during the three months immediately prior to the insurance's effective date.

The Long Term Disability Policy Provision

The LTD Policy states that “Benefits will not be paid for a Total Disability: (1) caused by; (2) contributed to by; or (3) resulting from; a Pre-Existing Condition unless the Insured has been Actively at Work for one (1) full day following the end of twelve (12) consecutive months from the date he/she became an Insured.”

A Pre-existing Condition is defined as “any Sickness or Injury for which the Insured received medical Treatment, consultation, care or services, including diagnostic procedures, or took prescribed drugs or medicines, during the three (3) months immediately prior to the Insured’s effective date of insurance.”

“Sickness” under the Policy “means illness or disease causing Total Disability which begins while insurance coverage is in effect for the Insured. Sickness includes pregnancy, childbirth, miscarriage, or any complications therefrom.”

Legal Context: What Do Pre-Existing Conditions in Disability Insurance Policies Mean?

Pre-existing condition clauses in disability insurance policies are designed to prevent individuals from obtaining coverage for medical conditions that existed before the long term disability policy’s effective date and caused disability shortly after becoming insured.

The pre-existing condition clause includes what is known as a “look-back period,” which is typically the 3 month period before the effective date of insurance. The insured does not qualify for long term disability benefits if she becomes disabled due to a condition that existed during the look back period.

These clauses typically exclude coverage for disabilities resulting from illnesses or injuries for which the insured received medical treatment, consultation, care, or services prior to the coverage start date. The intent is to limit coverage when an individual might only seek insurance upon knowing they have a condition that could lead to a disability claim.

The key legal question in this case revolved around whether the pre-existing condition substantially contributed to the disability and how directly the condition is linked to the claimed disability.

Dabdoub Law Firm's Advocacy on Behalf of Ms. Bradshaw

Reliance Standard’s case hinged on the idea that because Ms. Bradshaw treated for pregnancy during the look back period, the pre-existing condition exclusion should apply and thus, she is not entitled to benefits under the Policy.

Eddie Dabdoub argued that Reliance’s argument was a misapplication of the Policy terms because pregnancy did not cause Total Disability, as the pre-existing exclusion requires. Instead, stroke caused Total Disability and stroke was not treated for during the look back period.

Additionally, Reliance’s evidence that pregnancy contributed to Bradshaw’s stroke is irrelevant as the Policy asks what caused, contributed to, or resulted in Total Disability, not what caused, contributed to, or resulted in a condition, which itself caused, contributed to, or resulted in Total Disability.

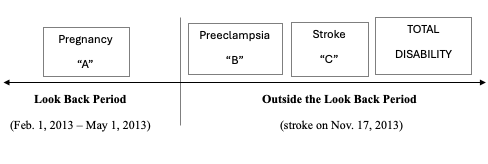

To help clarify, Dabdoub Law Firm supplied the chart below to the court for ease of reference on the timeline of her pregnancy, stroke, and disability.

As shown in the chart, the pregnancy itself was not disabling, but rather a series of events lead to disability, none of which existed during the look back period. Eddie Dabdoub explained to the court that the complications leading to her disability were not foreseeable and thus should not fall under the pre-existing condition exclusion. |

The Court's Ruling

The United States Court of Appeals for the Eleventh Circuit reviewed the case and found that Reliance Standard's denial of benefits was not reasonable. The court emphasized that for a pre-existing condition exclusion to apply, the condition must substantially contribute to the disability.

In Bradshaw's case, while her pregnancy existed before the policy's effective date, the specific complications leading to her disability were not present or treated during the look-back period defined in the policy. Therefore, the court concluded that the pre-existing condition exclusion was not applicable in this context. The decision reversed the district court’s ruling and remanded the case for further proceedings consistent with its opinion.

Implications of the Ruling

This case created a strong precedent in ERISA disability cases involving pre-existing condition arguments. Insurers rely heavily on the pre-existing limitation to avoid liability, but they are not always right.

Moreover, it the necessity for insurers to clearly define the scope and application of pre-existing condition exclusions in their policies. Ambiguities in policy language are typically construed in favor of the insured, especially under ERISA-governed plans.

For policyholders, this case highlights the importance of understanding the specific terms and definitions within their disability insurance policies, particularly concerning pre-existing conditions.

Ms. Bradshaw won her case and was paid her disability benefits as a result of her strong legal team at Dabdoub Law Firm. Their expertise in disability insurance law and deep understanding of the interplay between her medical conditions allowed them to defeat Reliance’s position that her disability was pre-existing.

Help from a Lawyer with Expertise in Disability Insurance

Disability insurance law is complex. Hiring an experienced long term disability attorney is important. Because all disability lawyers at this law firm focus on disability insurance claims, we have expertise in disability insurance law.

That means we have:

- Experience with every major disability insurance company;

- A proven track record of success by winning major disability lawsuits;

- Recovered millions of dollars in disability benefits for clients;

And, we never charge fees or costs unless our clients get paid.

The firm can help at any stage of your disability insurance claim, including:

- Submitting a disability insurance claim;

- Appealing a long-term disability denial;

- Negotiating a lump-sum settlement; or

- Filing a lawsuit against your disability insurance company.

Because federal law applies to most disability insurance claims, our lawyers are able to represent clients across the country.

Call to speak with an experienced disability attorney. Consultations are free.